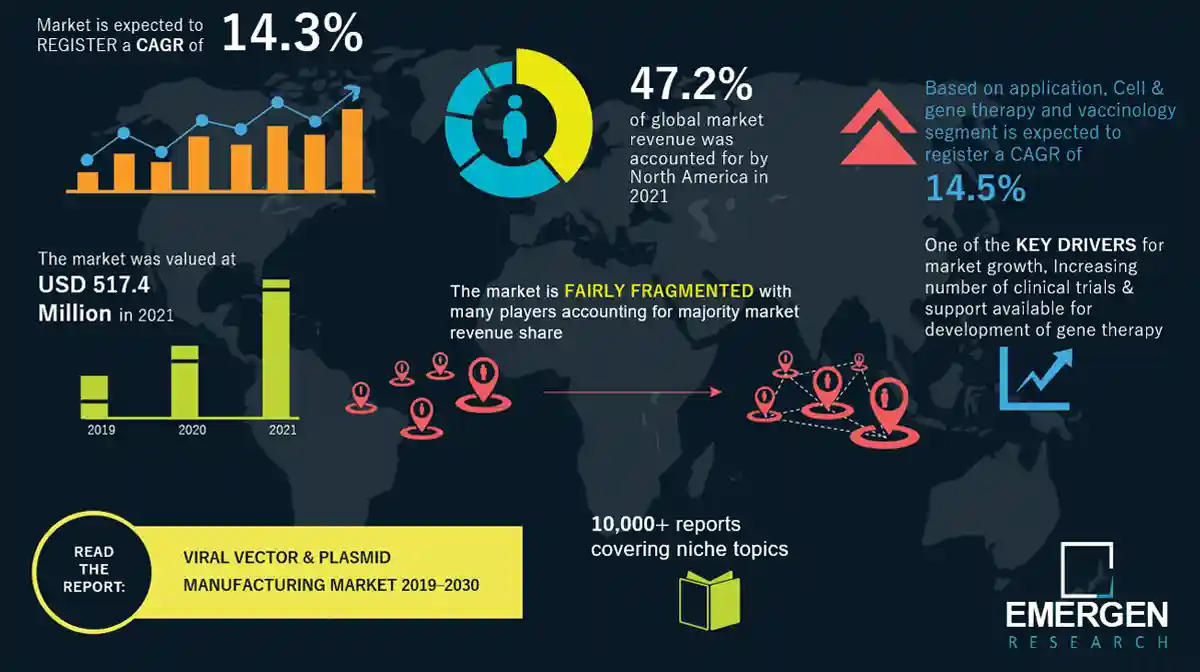

Global Viral Vector and Plasmid Manufacturing Market

The Global Viral Vector and Plasmid Manufacturing Market Report by Emergen Research offers extensive knowledge and information about the Viral Vector and Plasmid Manufacturing market pertaining to market size, market share, growth influencing factors, opportunities, and current and emerging trends. The report is formulated with the updated and latest information of the global Viral Vector and Plasmid Manufacturing market further validated and verified by the industry experts and professionals. The Global Viral Vector and Plasmid Manufacturing Market report contains historical, current, and forecast estimation of the revenue generation and profits for each segment and sub-segment of the Viral Vector and Plasmid Manufacturing market in each key region of the world. The report additionally sheds light on the emerging growth opportunities in the business sphere that are anticipated to bolster the growth of the market.

In today's competitive marketplace, staying ahead of the curve is essential for businesses of all sizes. Understanding consumer behavior, market trends, and emerging opportunities is crucial for making informed decisions and developing effective strategies. Emergen Research recognizes this need and has invested significant resources in developing a cutting-edge market research content library.

The newly launched Viral Vector and Plasmid Manufacturing market research content is meticulously crafted by industry experts, leveraging extensive data analysis, and a deep understanding of various markets. This rich collection includes in-depth reports, whitepapers, case studies, trend analyses, and industry insights covering a wide range of sectors, including but not limited to technology, healthcare, finance, consumer goods, and manufacturing.

Request Free Sample Copy (To Understand the Complete Structure of this Report [Summary + TOC]) @ https://www.emergenresearch.com/request-free-sample/14

The global Viral Vector and Plasmid Manufacturing Market size is estimated at USD 7.2 Billion in 2025, with strong expansion projected to reach USD 25 Billion by 2035, reflecting a CAGR of 13.5% over the forecast period.

This growth trajectory is structurally anchored in three high-impact forces:

-

Acceleration of Gene & Cell Therapy Pipelines

The number of advanced therapy medicinal products (ATMPs) is scaling rapidly, directly increasing demand for viral vectors (AAV, lentivirus) and plasmid DNA.

- As per U.S. Food and Drug Administration, over 2,000 active gene therapy clinical trials were ongoing globally by 2024, with a significant share requiring viral vector-based delivery systems.

- The Alliance for Regenerative Medicine reported $23+ billion in funding for cell and gene therapy companies in 2023, signaling sustained capital inflow into manufacturing-dependent pipelines.

Implication: Each clinical-stage therapy requires scalable GMP-grade vector production, creating a direct multiplier effect on manufacturing revenues.

-

Manufacturing Bottlenecks Driving Outsourcing & Capacity Expansion

Vector production remains a critical constraint due to low yields and complex bioprocessing.

- The U.S. National Institutes of Health highlights that AAV manufacturing yields can vary widely, often below 1E15 vg per batch, limiting commercial scalability.

- In response, contract development and manufacturing organizations (CDMOs) are expanding aggressively-e.g., multiple facilities exceeding 100,000+ sq. ft. of biomanufacturing space globally.

Implication: Persistent supply-demand imbalance is pushing premium pricing and long-term contracts, structurally elevating market value.

-

Regulatory and Policy Support for Advanced Therapies

Governments are actively accelerating approval pathways and funding frameworks.

- The European Medicines Agency has expanded PRIME (Priority Medicines) support for gene therapies, reducing time-to-market for novel biologics.

- In the U.S., regenerative medicine advanced therapy (RMAT) designations have increased steadily, enabling faster commercialization cycles.

Implication: Faster approvals translate into earlier manufacturing scale-up, compressing timelines and boosting annual demand for vectors and plasmids.

Industry Validation Signals

- Commercial gene therapies are scaling: Products like CAR-T and AAV-based therapies are transitioning from niche to multi-billion-dollar revenue categories.

- Biopharma CAPEX is rising: Major firms are committing >$1 billion per facility for next-generation biologics manufacturing infrastructure.

- Technology shifts: Adoption of suspension cell cultures and producer cell lines is improving yields, further enabling industrial-scale production.

Competitive Landscape:

The latest study provides an insightful analysis of the broad competitive landscape of the global Viral Vector and Plasmid Manufacturing market, emphasizing the key market rivals and their company profiles. A wide array of strategic initiatives, such as new business deals, mergers & acquisitions, collaborations, joint ventures, technological upgradation, and recent product launches, undertaken by these companies has been discussed in the report.

Rapid Expansion of Approved Gene Therapies Creating Immediate Manufacturing Demand

The commercialization wave of gene therapies is no longer theoretical—it is translating directly into recurring manufacturing demand.

- The U.S. Food and Drug Administration has approved 30+ gene and cell therapies as of 2024, with projections indicating 10–20 new approvals annually over the next few years.

- The National Institutes of Health estimates that ~80% of gene therapies rely on viral vectors (AAV, lentivirus) for delivery, making vector manufacturing a non-substitutable component of commercialization.

Why this driver exists:

Biopharma pipelines are transitioning from early-stage innovation to late-stage and commercial launches. Unlike small molecules, gene therapies require batch-specific, high-purity biological production—creating continuous manufacturing demand per therapy.

Revenue impact:

Each approved therapy requires:

- Clinical-to-commercial scale-up

- Repeated batch production for patient cohorts

- Lifecycle manufacturing (post-approval supply)

This results in multi-year manufacturing contracts, often locked with CDMOs, creating predictable revenue streams.

Strategic implication:

- Investors: Strong visibility on long-term cash flows due to locked manufacturing demand

- Companies: Early investment in scalable vector platforms becomes a competitive moat

Surge in Biopharma Outsourcing to Specialized CDMOs

Biopharmaceutical companies are increasingly outsourcing vector and plasmid production due to technical complexity and high capital requirements.

- According to United Nations Conference on Trade and Development, biopharmaceutical contract manufacturing has grown at >8% annually, with advanced biologics contributing a disproportionate share of this expansion.

- Building a GMP-compliant viral vector facility can exceed USD 200–500 million in capital expenditure, making outsourcing economically preferable for most mid-sized biotech firms.

Why this driver exists:

Viral vector manufacturing involves:

- Complex upstream cell culture systems

- Low-yield purification processes

- Stringent regulatory compliance (GMP, sterility, viral safety)

Most biotech firms lack in-house expertise and infrastructure, driving reliance on CDMOs.

Revenue impact:

- Long-term manufacturing agreements (5–10 years)

- Premium pricing due to limited global capacity

- High switching costs once process validation is completed

Strategic implication:

- Investors: CDMOs in this space command higher margins than traditional biologics manufacturing

- Companies: Strategic partnerships with CDMOs reduce time-to-market and capital risk

Technological Advancements Improving Yield and Scalability

Breakthroughs in vector production technologies are enabling industrial-scale manufacturing, unlocking previously constrained market potential.

- The European Commission has funded multiple bioprocess innovation programs under Horizon Europe, targeting 2–5x improvements in viral vector yield efficiency through advanced bioreactor systems.

- Adoption of suspension-based HEK293 cell cultures and producer cell lines is reducing batch variability and increasing volumetric productivity.

Why this driver exists:

Historically, low yields and inconsistent quality limited scalability. New process innovations are:

- Enhancing transfection efficiency

- Reducing contamination risks

- Enabling continuous manufacturing models

Revenue impact:

- Lower cost per dose: broader therapy adoption

- Higher throughput: increased production volumes

- Improved margins for manufacturers

Strategic implication:

- Investors: Technology-driven manufacturers will outperform capacity-only players

- Companies: Investing in proprietary production platforms creates differentiation and pricing power

Emergen Research is Offering a full report (Grab a Copy Now) @ https://www.emergenresearch.com/industry-report/viral-vector-and-plasmid-manufacturing-market

Market Segmentation:

The report bifurcates the Viral Vector and Plasmid Manufacturing market on the basis of different product types, applications, end-user industries, and key regions of the world where the market has already established its presence. The report accurately offers insights into the supply-demand ratio and production and consumption volume of each segment.

Top 10 Companies Viral Vector and Plasmid Manufacturing Market

- Lonza

- Thermo Fisher Scientific

- FUJIFILM Diosynth Biotechnologies

- AGC Biologics

- Catalent

- Aldevron

- Charles River Laboratories

- Resilience

- ProBio

- WuXi Biologics

Key Company Analysis

Lonza remains one of the strongest platform players because it combines CDMO scale with dedicated Cell & Gene Technologies capabilities in viral vectors, cell therapy, and plasmid-related process optimization. Lonza’s 2024 Annual Report states that its Cell & Gene Technologies business offers CDMO services across viral vector, cell therapy, and mRNA programs, while its recent technical publications also show active work on plasmid engineering and HEK293-based AAV productivity improvement. That matters strategically because Lonza is not competing only on capacity; it is competing on process performance, productivity, and platform repeatability.

Thermo Fisher Scientific is particularly well positioned in plasmid DNA because it has built an integrated raw-material-to-manufacturing offering. The company announced the opening of a 67,000-square-foot cGMP plasmid DNA manufacturing facility in Carlsbad, California, specifically to serve demand from plasmid-based therapies, cell and gene therapies, and mRNA-related programs. Its broader gene therapy manufacturing footprint also spans viral vector support services, giving it an advantage with customers that want fewer handoffs across development and supply.

FUJIFILM Diosynth Biotechnologies is differentiated by its effort to industrialize AAV manufacturing through platformization. The company states that its gene therapy network supports preclinical through commercial GMP manufacturing, and it offers off-the-shelf cGMP cell lines plus plasmid toolboxes designed for commercial-ready rAAV production. Its platform materials highlight high-titer suspension HEK293 systems and a modular approach aimed at reducing development timelines and de-risking scale-up. In commercial terms, that gives FUJIFILM an advantage with sponsors seeking faster tech transfer and more predictable late-phase manufacturing.

AGC Biologics is emerging as a particularly relevant lentiviral specialist. The company markets full-service viral vector capabilities across AAV, lentiviral, and retroviral vectors, and in January 2025 announced that its Milan site would prepare commercial lentiviral vector manufacturing for Adaptimmune’s lete-cel product. It also promotes its ProntoLVV platform as a way to shorten the path to GMP, which signals a clear strategy: win on speed, template-driven execution, and readiness for commercial cell therapy demand rather than competing only as a generalist biologics CDMO.

Aldevron continues to hold a strong strategic position in plasmid DNA, especially as upstream bottlenecks become more visible. Aldevron describes plasmid DNA as a critical bottleneck in advanced therapeutics and has continued expanding its customer-facing infrastructure, including a new discovery center in Waltham announced in July 2025. Backed by Danaher, Aldevron’s advantage is less about being the broadest CGT player and more about being deeply associated with high-quality plasmid DNA and other starting materials that sit upstream of viral vector production. That makes it commercially important even when it is not the final vector manufacturer of record.

Our goal at Emergen Research is to empower businesses with the knowledge and insights necessary to make informed decisions and thrive in today's dynamic business landscape. Our market research content is designed to equip professionals and organizations with comprehensive analyses, actionable recommendations, and a competitive edge to achieve their growth objectives.

The global Viral Vector and Plasmid Manufacturing Market size is estimated at USD 7.2 Billion in 2025, with strong expansion projected to reach USD 25 Billion by 2035, reflecting a CAGR of 13.5% over the forecast period.

This growth trajectory is structurally anchored in three high-impact forces:

-

Acceleration of Gene & Cell Therapy Pipelines

The number of advanced therapy medicinal products (ATMPs) is scaling rapidly, directly increasing demand for viral vectors (AAV, lentivirus) and plasmid DNA.

- As per U.S. Food and Drug Administration, over 2,000 active gene therapy clinical trials were ongoing globally by 2024, with a significant share requiring viral vector-based delivery systems.

- The Alliance for Regenerative Medicine reported $23+ billion in funding for cell and gene therapy companies in 2023, signaling sustained capital inflow into manufacturing-dependent pipelines.

Implication: Each clinical-stage therapy requires scalable GMP-grade vector production, creating a direct multiplier effect on manufacturing revenues.

-

Manufacturing Bottlenecks Driving Outsourcing & Capacity Expansion

Vector production remains a critical constraint due to low yields and complex bioprocessing.

- The U.S. National Institutes of Health highlights that AAV manufacturing yields can vary widely, often below 1E15 vg per batch, limiting commercial scalability.

- In response, contract development and manufacturing organizations (CDMOs) are expanding aggressively-e.g., multiple facilities exceeding 100,000+ sq. ft. of biomanufacturing space globally.

Implication: Persistent supply-demand imbalance is pushing premium pricing and long-term contracts, structurally elevating market value.

-

Regulatory and Policy Support for Advanced Therapies

Governments are actively accelerating approval pathways and funding frameworks.

- The European Medicines Agency has expanded PRIME (Priority Medicines) support for gene therapies, reducing time-to-market for novel biologics.

- In the U.S., regenerative medicine advanced therapy (RMAT) designations have increased steadily, enabling faster commercialization cycles.

Implication: Faster approvals translate into earlier manufacturing scale-up, compressing timelines and boosting annual demand for vectors and plasmids.

Industry Validation Signals

- Commercial gene therapies are scaling: Products like CAR-T and AAV-based therapies are transitioning from niche to multi-billion-dollar revenue categories.

- Biopharma CAPEX is rising: Major firms are committing >$1 billion per facility for next-generation biologics manufacturing infrastructure.

- Technology shifts: Adoption of suspension cell cultures and producer cell lines is improving yields, further enabling industrial-scale production.

Custom Requirements can be requested for this Report [Customization Available] @ https://www.emergenresearch.com/request-for-customization/14

The Viral Vector and Plasmid Manufacturing Market is structured across the following key dimensions:

-

By Type Outlook (Revenue, USD Million; 2024-2034)

- Viral Vectors (AAV, Lentivirus, Retrovirus, Adenovirus)

- Plasmid DNA

-

By Application Outlook (Revenue, USD Million; 2024-2034)

- Gene Therapy

- Cell Therapy (e.g., CAR-T)

- Vaccinology

- Research Use

-

By End-use Outlook (Revenue, USD Million; 2024-2034)

- Biopharmaceutical Companies

- Contract Development & Manufacturing Organizations (CDMOs)

- Academic & Research Institutes

-

By Technology Outlook (Revenue, USD Million; 2024-2034)

- Transient Transfection

- Stable Producer Cell Lines

- Suspension Cell Culture Systems

-

Regional Outlook (Revenue, USD Million; 2024–2034)

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Benelux

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Rest of APAC

- Latin America

- Brazil

- Rest of LATAM

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Turkey

- Rest of MEA

- North America

Target Audience of the Global Viral Vector and Plasmid Manufacturing Market Report:

- Key Market Players

- Investors

- Venture capitalists

- Small- and medium-sized and large enterprises

- Third-party knowledge providers

- Value-Added Resellers (VARs)

- Global market producers, distributors, traders, and suppliers

- Research organizations, consulting companies, and various alliances interested in this sector

- Government bodies, independent regulatory authorities, and policymakers

Key features and benefits of Emergen Research's market research content include:

- Comprehensive Analysis: Each piece of content is meticulously researched and provides a detailed analysis of market trends, competitive landscape, consumer behavior, and emerging opportunities. Businesses can leverage this information to identify untapped markets, devise effective marketing strategies, and make data-driven decisions.

- Actionable Recommendations: The market research content provides practical insights and actionable recommendations to help businesses enhance their products, services, and overall customer experience. These recommendations are tailored to the specific needs and challenges of each industry, allowing companies to implement strategies that drive growth and profitability.

- Expert Insights: Emergen Research's team of industry experts and analysts contribute their in-depth knowledge and expertise to every piece of content. Their insights shed light on industry-specific challenges, best practices, and emerging trends, helping businesses stay ahead of the competition and seize new opportunities.

- Timely Updates: The market research content is regularly updated to reflect the latest market trends and dynamics. Subscribers will have access to the most up-to-date information, enabling them to adapt their strategies and stay relevant in today's rapidly evolving business environment.

The global Viral Vector and Plasmid Manufacturing Market size is estimated at USD 7.2 Billion in 2025, with strong expansion projected to reach USD 25 Billion by 2035, reflecting a CAGR of 13.5% over the forecast period.

This growth trajectory is structurally anchored in three high-impact forces:

-

Acceleration of Gene & Cell Therapy Pipelines

The number of advanced therapy medicinal products (ATMPs) is scaling rapidly, directly increasing demand for viral vectors (AAV, lentivirus) and plasmid DNA.

- As per U.S. Food and Drug Administration, over 2,000 active gene therapy clinical trials were ongoing globally by 2024, with a significant share requiring viral vector-based delivery systems.

- The Alliance for Regenerative Medicine reported $23+ billion in funding for cell and gene therapy companies in 2023, signaling sustained capital inflow into manufacturing-dependent pipelines.

Implication: Each clinical-stage therapy requires scalable GMP-grade vector production, creating a direct multiplier effect on manufacturing revenues.

-

Manufacturing Bottlenecks Driving Outsourcing & Capacity Expansion

Vector production remains a critical constraint due to low yields and complex bioprocessing.

- The U.S. National Institutes of Health highlights that AAV manufacturing yields can vary widely, often below 1E15 vg per batch, limiting commercial scalability.

- In response, contract development and manufacturing organizations (CDMOs) are expanding aggressively-e.g., multiple facilities exceeding 100,000+ sq. ft. of biomanufacturing space globally.

Implication: Persistent supply-demand imbalance is pushing premium pricing and long-term contracts, structurally elevating market value.

-

Regulatory and Policy Support for Advanced Therapies

Governments are actively accelerating approval pathways and funding frameworks.

- The European Medicines Agency has expanded PRIME (Priority Medicines) support for gene therapies, reducing time-to-market for novel biologics.

- In the U.S., regenerative medicine advanced therapy (RMAT) designations have increased steadily, enabling faster commercialization cycles.

Implication: Faster approvals translate into earlier manufacturing scale-up, compressing timelines and boosting annual demand for vectors and plasmids.

Industry Validation Signals

- Commercial gene therapies are scaling: Products like CAR-T and AAV-based therapies are transitioning from niche to multi-billion-dollar revenue categories.

- Biopharma CAPEX is rising: Major firms are committing >$1 billion per facility for next-generation biologics manufacturing infrastructure.

- Technology shifts: Adoption of suspension cell cultures and producer cell lines is improving yields, further enabling industrial-scale production.

Key Questions Answered in the Report:

- What is the growth rate of the Viral Vector and Plasmid Manufacturing market? What is the anticipated market valuation of Viral Vector and Plasmid Manufacturing industry by 2034?

- What are the key growth driving and restraining factors of the Viral Vector and Plasmid Manufacturing market?

- Who are the prominent players operating in the market? What are the key strategies adopted by these companies?

- What are the key opportunities and growth prospects of the Viral Vector and Plasmid Manufacturing industry over the forecast period?

- Which region is expected to show significant growth in the coming years?

About Emergen Research

Emergen Research is a market research and consulting company that provides syndicated research reports, customized research reports, and consulting services. Our solutions purely focus on your purpose to locate, target, and analyze consumer behavior shifts across demographics, across industries, and help clients make smarter business decisions. We offer market intelligence studies ensuring relevant and fact-based research across multiple industries, including Healthcare, Touch Points, Chemicals, Types, and Energy.

Contact Us:

Eric Lee

Corporate Sales Specialist

Emergen Research | Web: https://www.emergenresearch.com/

Direct Line: +1 (604) 757-9756

E-mail: sales@emergenresearch.com